Reits Picking Guide

REITs, or real estate investment trusts, are companies that own or finance income-producing real estate across a range of property sectors. These real estate companies have to meet a number of requirements to qualify as REITs. Most REITs trade on major stock exchanges, and they offer a number of benefits to investors.

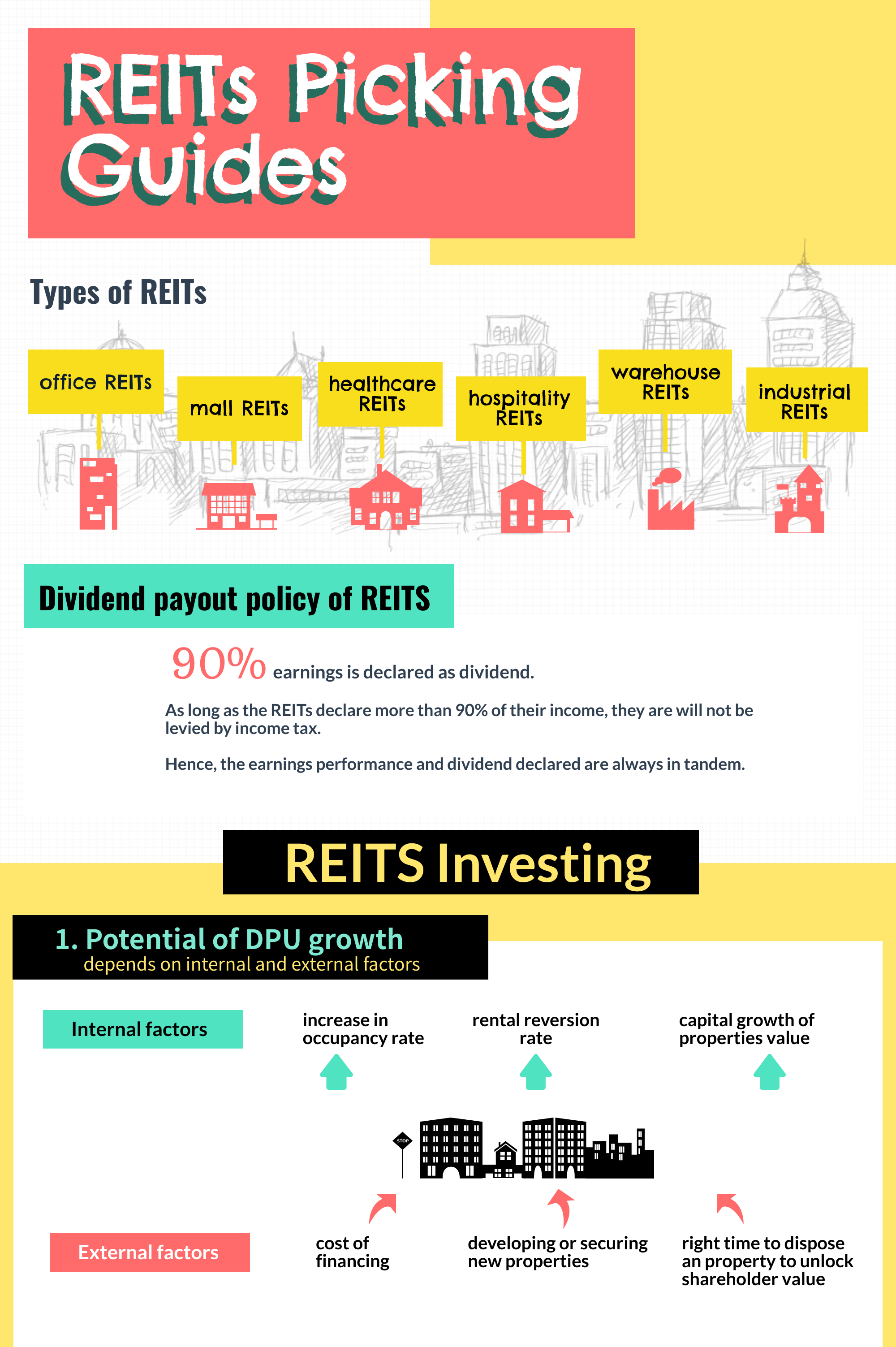

Real Estate Investment Trust, which is also known as REIT, is a tool that every dividend investors love. REITs are obliged to distribute 90% of their earning, hence the earnings performance and dividend declared are always in tandem. There are office REITs, mall REITs, healthcare REITs, warehouse REITs, industrial REITs, and hospitality REITs. REITs can be a cheap and effective way if you would like to involve in the property market. However, not every REIT behaves in the same way. Here are the 7 things you should take note of when investing in REITs.

Potential of DPU growth

The growth potential of the Dividend per Unit (DPU) depends on both internal and external factors.

Internal factor relies on an increase in occupancy rate, rental reversion rate and capital growth of properties value. This can be done via renovation and refitting, a marketing campaign to increase foot traffic, and efficient cost control by management.

External factors rely on management expertise on the cost of financing, accessibility to easy credit, management capability on developing or securing new properties, and the right time to dispose of a property to unlock shareholder value.

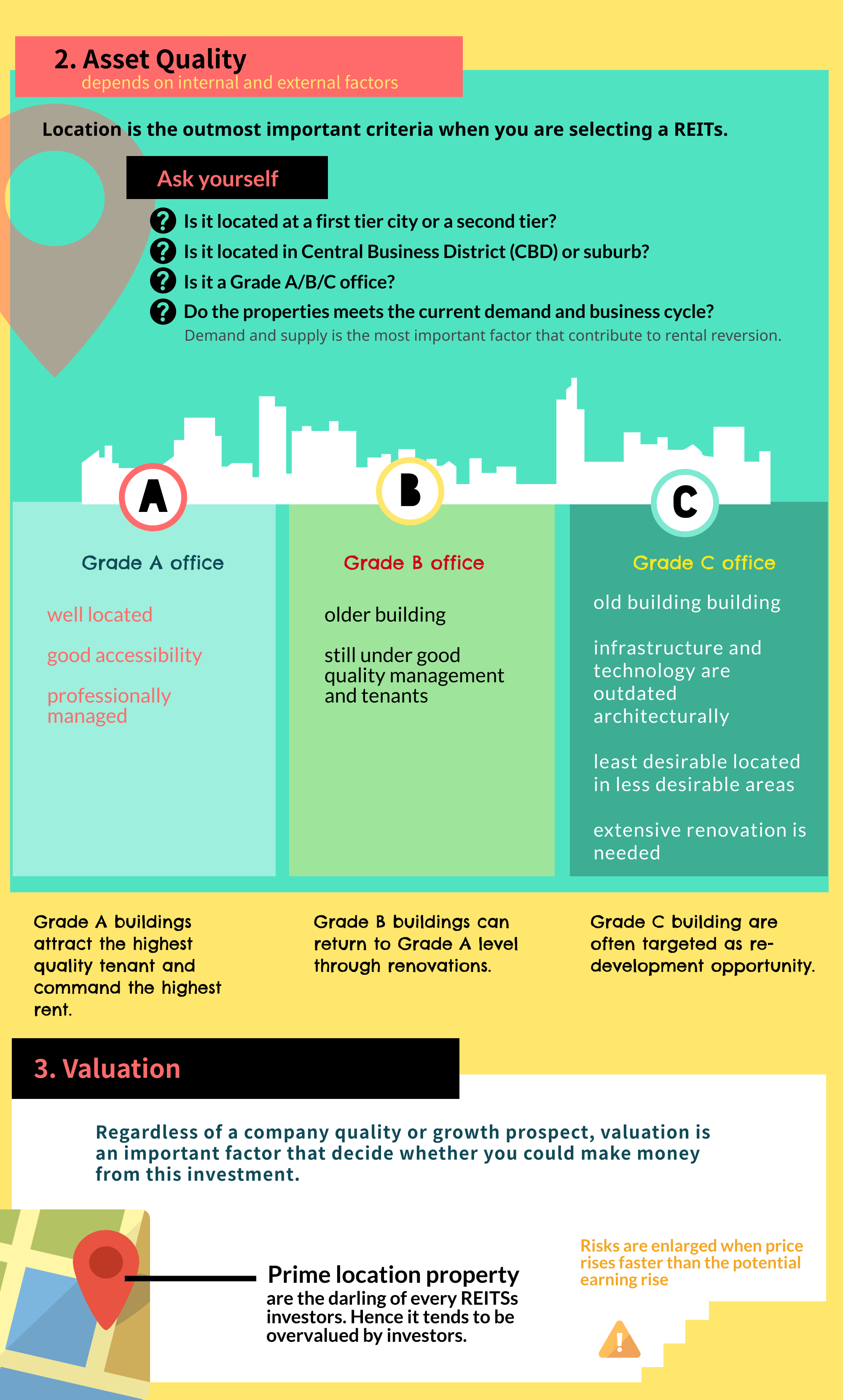

Asset Quality

Location is the utmost important criterion when you are selecting a REIT.

Is it located in a first-tier city or a second tier?

Is it located in Central Business District (CBD) or suburb?

Is it a Grade A/B/C office? Grade A offices are well located, good accessibility, and professionally managed. They attract the highest quality tenant and command the highest rent. Grade B is older but still has good quality management and tenants. Grade B buildings can return to Grade A through renovations. Grade C offices are old buildings located in less desirable areas and often need extensive renovation. Their building infrastructure and technology are outdated and architecturally least desirable. However, Grade C buildings are often targeted as re-development opportunities.

Are the properties meet the current demand and business cycle? Demand and supply is the most important factor that contributes to rental reversion.

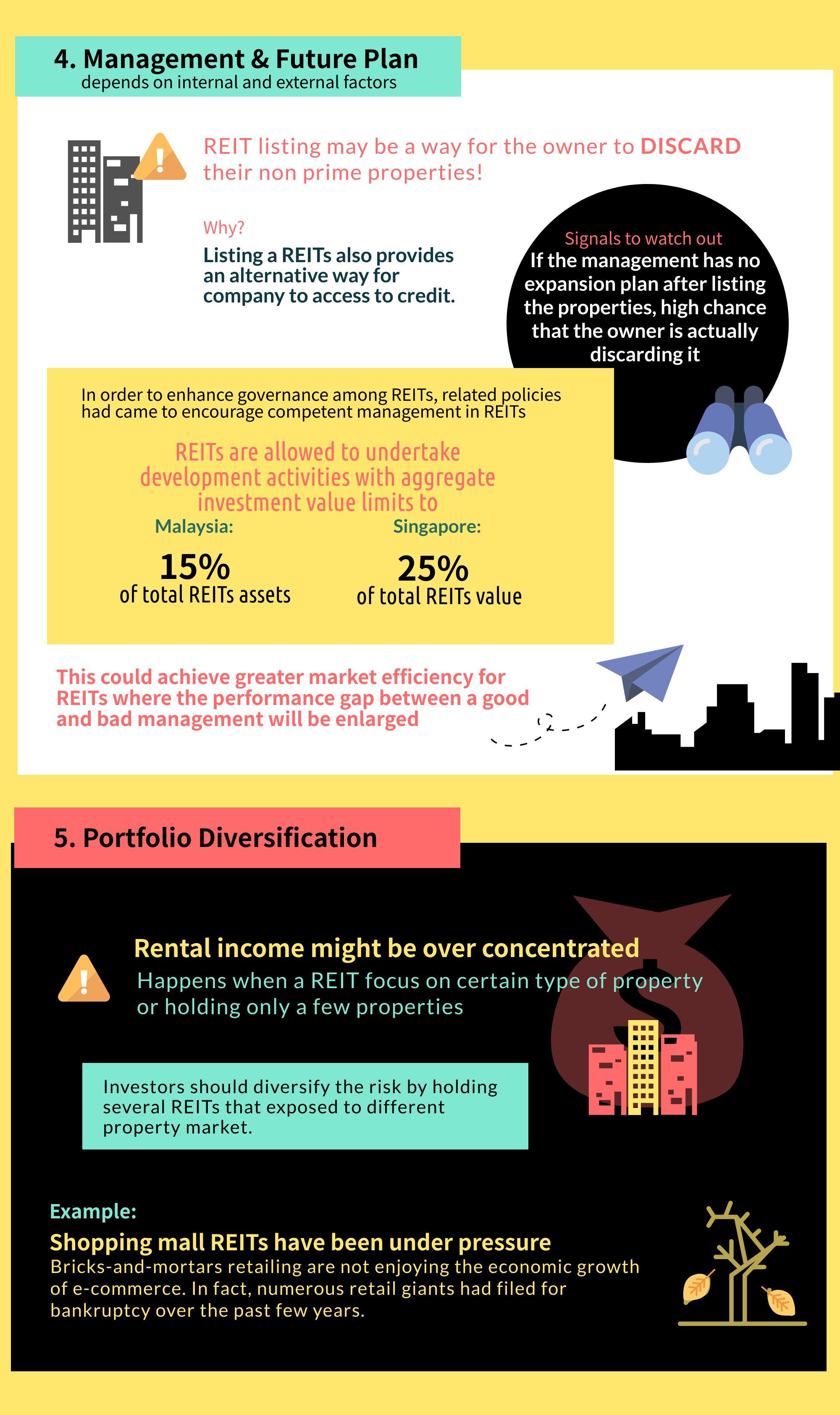

Management and future expansion plan

Listing a company comes with a cost but provides an alternative way for the company to access credit. If the management has no expansion plan in mind, listing the REIT may only be a way for the previous building owner to discard their non-prime property.

REITs are allowed to undertake property development activities (including the acquisition of vacant land). Singapore has a ceiling of 25% of the REITs value while Malaysia has a ceiling of 15%. With rules relaxing, a REIT with a strong future expansion plan and competent management will surely add more value to the REIT.

Information is accurate as of May 2021

Valuation

Regardless of a company's quality or growth prospect, valuation is an important factor that decides whether you could make money from this investment. Prime location property is the darling of every REIT investor. However, investors should be aware that when the price is rising so much faster than the potential earning rise, your risk is enlarged as well.

Portfolio Diversification

When a REIT focuses on a certain type of property or holding only a few properties, its rental income may be over-concentrated. Investors should diversify the risk yourself by holding several REITs that are exposed to the different property markets.

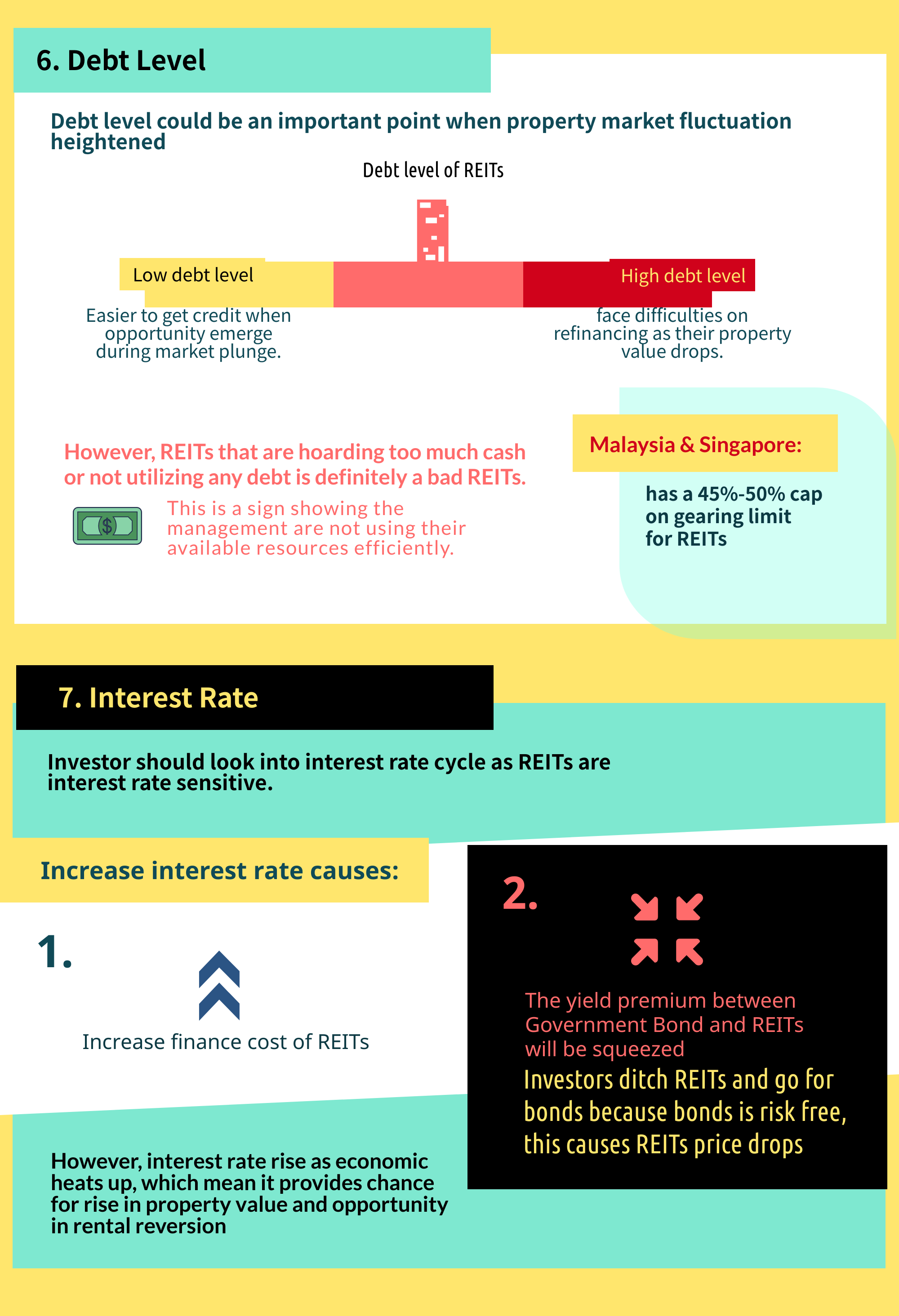

Debt Level

Debt level could be an important level when market fluctuation heightened. High debt level REITs could face difficulties on refinancing as their property value drops.

REITs with low debt levels could get credit more easily when opportunities emerge during the market plunge.

Malaysia has a 50% cap on leverage limit for REITs. (Due to Covid-19 pandemic, the Securities Commission (SC) of Malaysia has temporary increase the gearing limit for REITs in Malaysia to 60%, effective until 31 Dec 2022)

Singapore has a 45% cap on leverage limit for REITs. (Due to the Covid-19 pandemic, the Monetary Authority of Singapore (MAS) has increased the gearing limit for REITs in Malaysia to 50%)

However, REITs that are hoarding too much cash or not utilizing any debt are definitely bad REITs as the management are not using all their available resources efficiently.

Information is accurate as of May 2021

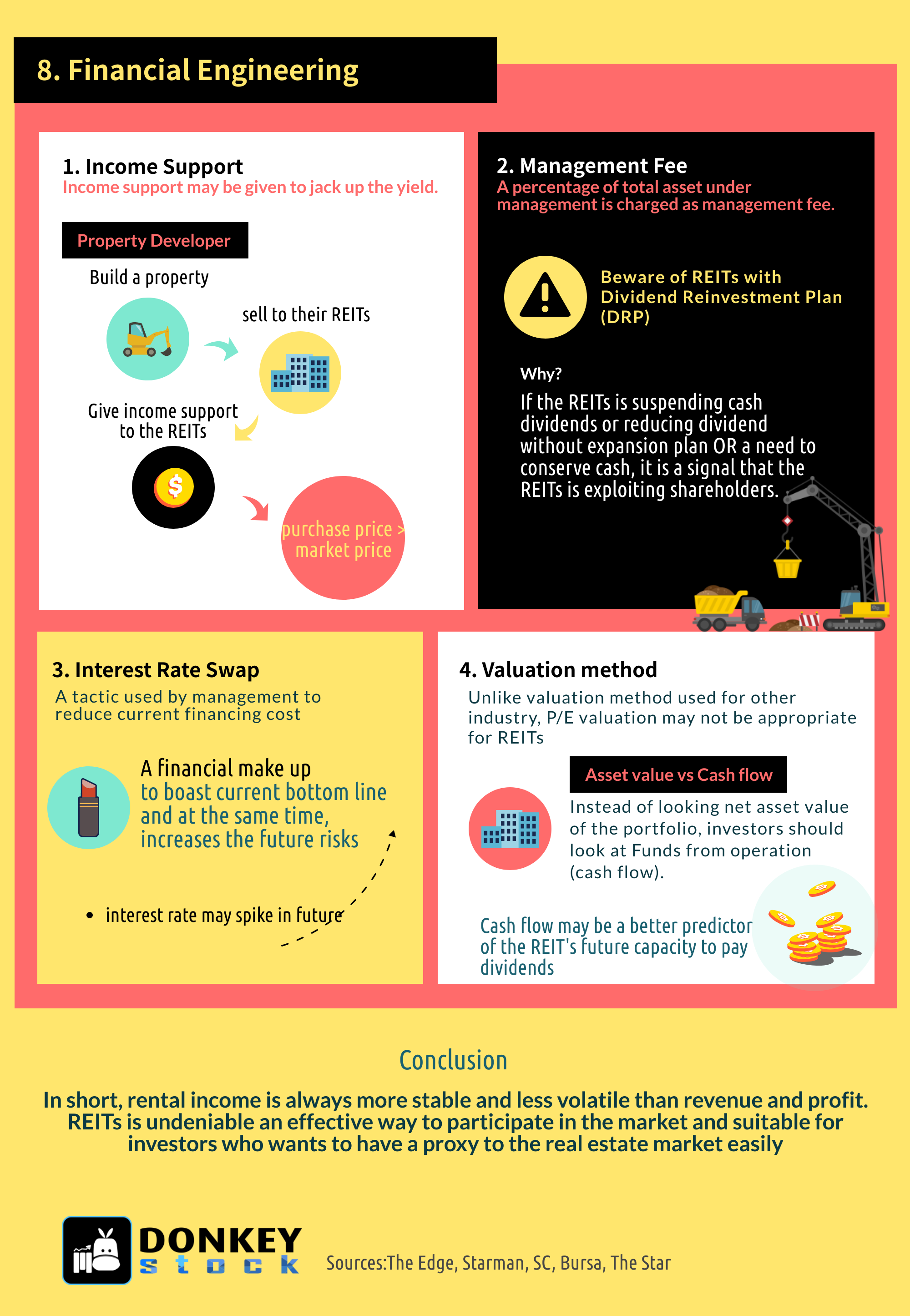

Financial Engineering

Income support may be given to jack up the yield. This occurs when a developer builds a property and sells it to their REIT. To ensure the shareholders of the REIT approve the purchase of the property, income support is ensured to make the acquisition of property lucrative. However, the purchase price is usually much higher than the market price

Management using a lot of Interest Rate swaps to reduce current financing costs. This may be a financial makeup that the management used to boast the current bottom line ignoring future risk.

As most management charge a percentage of total asset under management as their management fee, some management might introduce Dividend Reinvestment Plan (DRP) when there is no plans to expand or no desire need to conserve cash. This is only tactic management hopes to get a bigger share of management fee by exploiting the shareholders.

P/E may not be useful for REITs. Earnings may be misleading as property revaluation are gain are not a cash item

Conclusion

Do note that an interest rate hike would increase the finance cost of REITs. The yield premium between Government Bond and REITs will also be squeezed causing investors to ditch REITs and go for bonds. This causes REITs' prices to drop.

However, interest rise when the economy is overheating which provides an opportunity for a rental hike and capital appreciation in property value.

In short, rental income is always more stable and less volatile than sales or earnings. REITs are undeniable an effective way to participate in the market and suitable for investors who want to have a proxy to the real estate market easily.

Related Guides

Mental for Value Investing

2022-01-18

|

Guide

|

Tags: Portfolio

Value investing is an investment strategy that involves picking stocks that appear to be trading for less than their intrinsic or book value.

Types of yield curve and its impact to the market

2021-11-26

|

Guide

|

Tags: Portfolio

Yield Curve is a graph that shows how bond yields and maturities are related. Here are the types of the yield curve, factors affecting the yield curve and how the market interpret the different type of yield curve

Types of Coal

2021-11-25

|

Guide

|

Tags: Portfolio

Coal is an abundant natural resource that can be used as a source of energy and is primarily used as fuel to generate electric power. The article illustrates the major types or ranks of coal