Relationship between China economy and agriculture price

1 May, 2020

Category: Basic Materials

Tags: Portfolio

How a slowing down China's economy can drag down agriculture prices.

On 21 Apr 2020, China announced its Q1 2020 GDP growth rate.

During this period, China's GDP contracts 6.8%, the first contraction since 1992,

when the country began releasing such figures.

On the same day, investors saw oil price plunge, fearing a

further decrease in demand for fossil fuel from the world second-largest

economy. Oil prices have been the headlines of major financial media, resulting

in most investors missing out on the fact that most agriculture prices have started

another round of falling since that day.

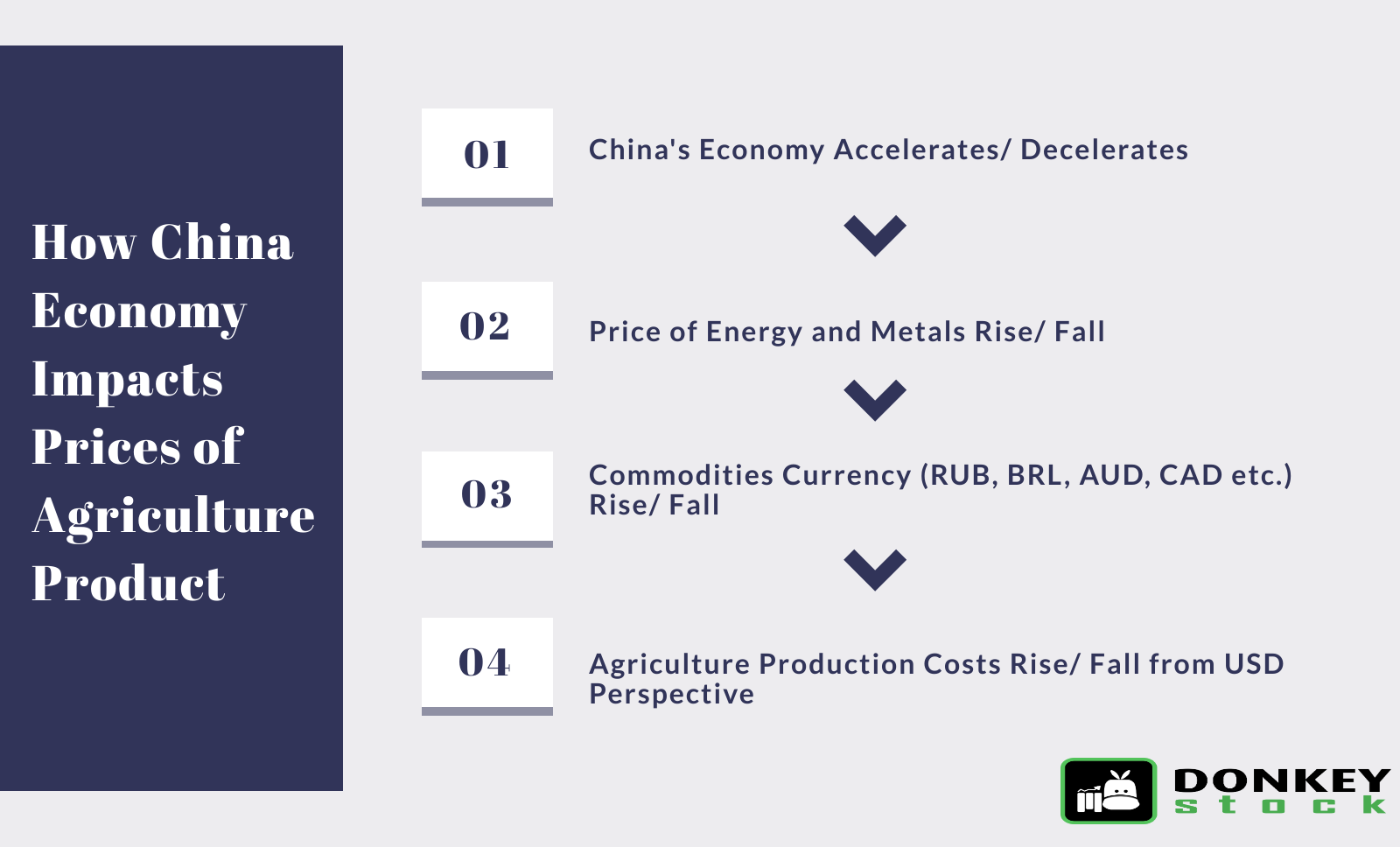

Hereby we explain why a slowdown in China economy serves as

a pulling factor for agriculture products price.

China, a fast-growing economy, relies on foreign resources

to fuel its economic growth. Although China is also one of the major

oil-producing countries, its production is insufficient to cater to the demand

for its domestic consumption. In 2018, China had overtaken the United States as

the worlds largest crude oil importer. Besides energy, China is also the

largest importer of industrial metals. In 2019, China has accounted for a 65%

share of the total global iron ore imports based on value.

This situation has made the countries that export energy

and metals to China highly reliant on China's economic growth rate. Those

countries include Russia, Brazil, Australia, and Canada. When China's economy

decelerates, the prices of energy and metals fall. As a result, the fall in

export value for these commodities creates lesser USD income for the countries

as mentioned, resulting in a fall in their local currency compared towards USD.

Coincidently, these countries are the world's major

agriculture product producers. When the local currency falls, the cost of

producing these agricultural products becomes lower from the US Dollar

perspective. Hence, the fall in agriculture prices.