Malaysia 10 years bond sell-off

27 Apr, 2022

Category: Bond

Tags: MGS

What is the implication of Malaysia 10 years bond sell-off to other asset classes.

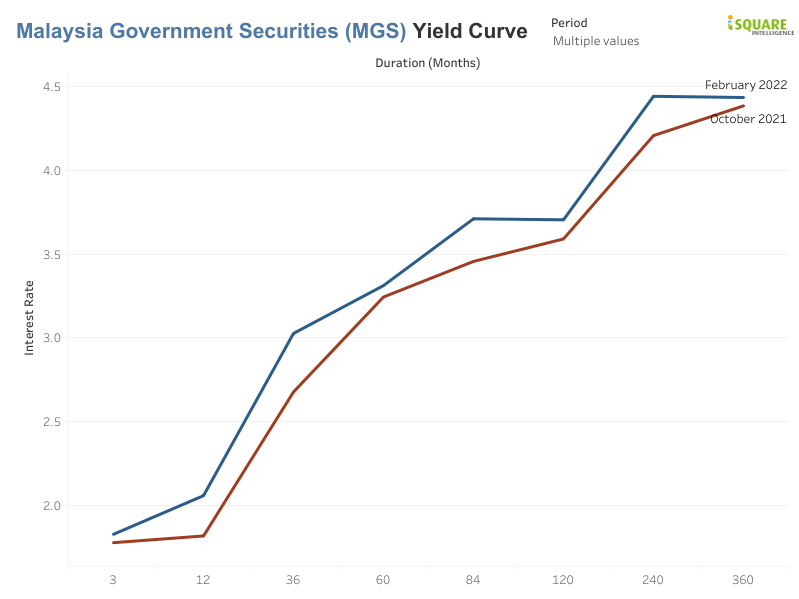

The Malaysian bond market registered a foreign net outflow of RM4.1 billion Malaysian Government Securities (MGS) and Government Investment Issues (GII) in March 2022.

If you look at the bond prices of Malaysia 10 years bonds, the sell-off started around 22 March and has accelerated in April. (A higher interest rate means a lower bond price). We believe the figures for Apr will look really bad.

The sharp outflow came amid a broad selloff in global bond markets last month, triggered by more aggressive monetary policy tightening signaled by the US Federal Reserve. The Fed now foresees six more 25 basis points (bps) hikes through the rest of the year, a sharp acceleration from its previous expectation of just two additional rate hikes.

But what is the implication of this sell-off?

Short-term rates are heavily influenced by the choices of the Central Bank while Long-term rates are usually the barometers of investors’ outlook for economic growth and inflation. With very long-term bonds, like 30-year issues, uncertainties are greater, so many focus their attention on the 10-year bond instead. The result is that the 10-year bond is used as the benchmark for the cost of risk-free borrowing and its rate is used to price trillions worth of other securities, including stocks or corporate loans.

A rise in the 10-year yield can therefore be bad for stocks, because investors may have less to gain from taking on more risk. It can also undermine stock prices by delivering a hit to discounted values of company cash flows. That’s especially true for growth stocks -- heavily represented by tech firms -- given that much of their income streams are expected well in the future.

In short, avoiding unprofitable growth companies and avoiding long-maturity securities is a way to keep your exposure to a rising bond yield.

Related Articles

The Malaysia yield curve is starting to invert

2023-08-09

|

Bond

|

Tags: Yield Curve

Something is brewing as Malaysia's yield curve had turned inverted.