Inari Amertron - Value emerges?

27 Jan, 2022

Category: Semiconductor

Tags: Inari Amertron

Can investors catch this falling knife after a 25% share plunge in a short period of time?

Inari Ametron has fallen 25% from its peak. Currently, the share price is hovering around the level where Inari raised cash via private placement in July 2021. Has value emerged for this company? Should I catch the falling knife?

We are not doing a peer comparison for this company as the valuation of its peer is also falling due to the market risk-off mood. We are also not using a discounted cash flow method because we do not know how high the interest rate can go.

We are gauging Inari based on the historical multiples.

Looking at its Price to Book Ratio (P/B), its valuation has back to its historical mean, but not yet in the cheap territory.

Looking at its Price to Earnings Ratio (P/E), its valuation looks even more expensive compared to its historical average.

In short, Inari current price is still not cheap enough for me to catch the falling knife. It may rebound, but if your goal is to invest in this good company for the long term at a cheap price, this is not the price level you should be looking at.

Related Articles

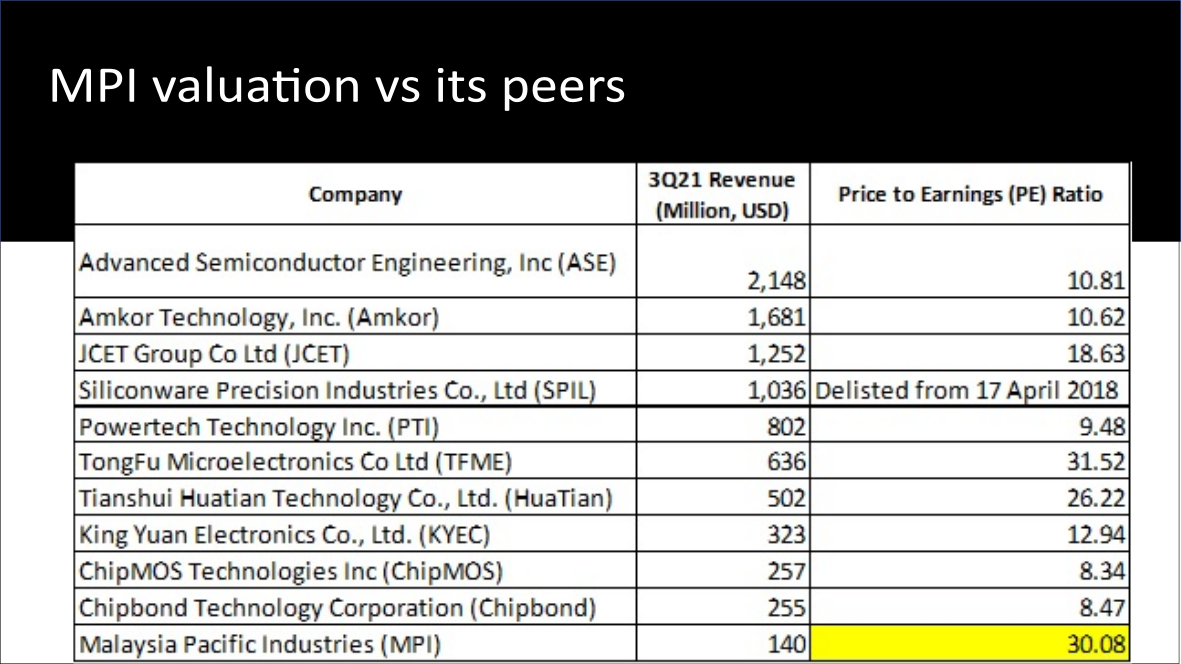

Malaysia Pacific Industries (MPI) and its Peer

2023-08-09

|

Semiconductor

|

Tags: Portfolio

A quick glimpse comparing the valuation of Malaysia Pacific Industries (MPI) and its major counterpart

为什么这次Nvidia收购Arm会遭到反对呢?

2023-08-09

|

Semiconductor

|

Tags: Nvidia, Arm

从技术路线的关系明白英伟达为什么想收购Arm

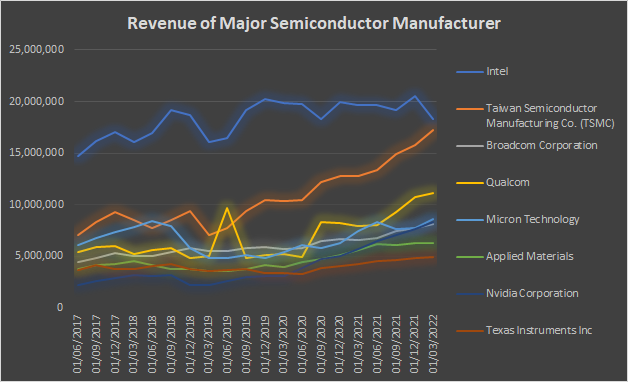

Comparison of Revenue of major semiconductor manufacturers

2023-08-09

|

Semiconductor

|

Tags: Semiconductor

Intel weak share price performance is substantiated by its stagnant revenue